Why are debt mutual funds more tax-efficient than fixed deposits?

I have nearly 60% of my financial assets’ portfolio in equity instruments. I use fixed deposits to build safety in my portfolio. I am aware that debt mutual funds have an edge over FDs in terms of tax treatment. How exactly does the tax treatment of FDs differ from debt mutual funds? Will it have a material impact on my portfolio considering fixed income instruments are moderate-growth & low-risk?

Fixed deposits have been India’s most favoured investment instrument for generations. It has been a steadfast member of the invincible trio of Indian investments together with gold and real estate. However, the ease of investing in fixed deposits combined with the moderate, yet reliable returns they offer often make us oblivious to the value erosion FDs suffer due to taxation.

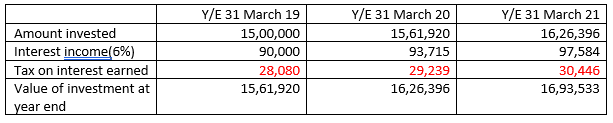

The longer the tenure you stay invested, the more pronounced is the difference between taxes incurred on FDs and debt mutual funds. If you are in the 30% tax bracket and had decided to invest Rs.15,00,000 on 1 April 2018, depending on whether you chose FDs or debt mutual funds, your after-tax returns will be as follows. Assume that the FDs offered a 6% coupon and that the debt funds delivered a 6% rate of return.

We have illustrated below, how these differences arise.

Tax treatment of interest income from FDs

Assume you are in the 30% marginal tax slab and are not liable to pay surcharges. Any interest income your FD portfolio generate will be taxed at *30% regardless of whether you reinvest this interest income or not.

*Marginal tax rate inclusive of cess @31.2%

Tax treatment of capital gains on debt mutual funds

If you had invested the same in a debt mutual fund giving the same rate of return, the investment would have grown as shown below:

*NAV on 01 April 2018: Rs. 2194.84

** NAV on 01 April 2021: Rs. 2614.09

Debt fund investments are not subject to taxation till you sell them. This makes them superior investment instruments relative to your savings bank accounts, fixed deposits and recurring deposits.

What happens upon the sale of debt funds? The tax impact depends on the period over which you remained invested in it.

- Holding period< 3 years (returns will be taxed at your marginal tax slab)

If the debt fund investment in the above example is liquidated on 30 March 2021(less than 3 years), the capital gains will be taxed at 31.2%. Assuming the value of the investment is Rs.17,86,524 on 30 March 2021, capital gains will amount to Rs. 2,86,524.

Short term capital gains tax incurred = 31.2% * 2,86,524

=Rs. 89,395

After-tax returns on debt mutual funds = Rs. 2,86,524-Rs. 89,395

= Rs,1,97,129/-

- Holding period >/= 3 years: capital gains adjusted for indexation will be taxed at 20%

Debt mutual funds’ tax efficiency over traditional investments like FDs steepen when holding period exceeds three years or more.

This advantage stems from the provision which permits an investor to adjust the cost price(NAV) at which he acquired the debt mutual fund for inflation as reflected in the cost inflation index (CII). A part of the capital gains the investor made over the holding period is likely to be inflation induced. The provision of indexation aims to relieve the investors of tax burden on the fraction of capital gains that is merely a reflection of inflation in the economy.

If the above debt mutual fund is redeemed on 01 April 2021, capital gains will be computed as follows:

Number of units purchased on 1 April 2018= Rs. 15,00,000/Rs. 2194.84

=683.42 units

Indexed cost of acquisition per unit = 2194.84* (CII for 2018-19/CII for 2021-22)

= 2194.84* (316/280)

=Rs. 2,477.03

Long term capital gains per unit = NAV on 01 April 2021- Indexed NAV on 01 April 2018

= Rs. 2,614.09 – Rs. 2,477.03

=Rs. 137.05

LTCG tax on total investment =20%*683.42 units *Rs.137.05

=Rs.18,733

After-tax returns on debt mutual funds = Rs. 2,86,524- Rs.18,733

= Rs.2,67,791

Thus, the after-tax returns of debt funds and fixed deposits over different holding periods varied as follows:

The tax advantage debt funds hold over fixed deposits will thus have a significant impact on your portfolio’s value over the long term.

By Aparna M

Financial Advisor – PeakAlpha Investments