On July 1, 2020 onwards, all shares and mutual fund purchases (except ETFs) will attract a stamp duty of 0.005%, and any transfer of mutual fund units will attract a stamp duty of 0.015%. Please read on for further details.

1. What is the rate of stamp duty?

As per SEBI regulations, 0.005% stamp duty will be levied on any mutual fund transaction that leads to creation of new units. The duty will apply to all mutual funds—both equity and debt. In absolute terms, the stamp duty amounts to ₹5 per ₹1,00,000 invested.

2. How is it calculated?

The stamp duty will be auto deducted by the registrar and transfer agent (RTA) of the mutual fund when you buy units. You do not have to pay it separately. The calculation is as shown below:

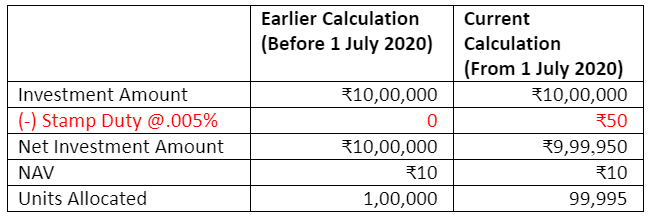

If you invest ₹10 lakhs in a mutual fund scheme with a NAV of ₹10, there will be a deduction of ₹50 (0.005% of ₹10 lakhs) towards stamp duty, and the remaining ₹9,99,950 will get invested.

In other words, you will be allotted 99,995 units (₹9,99,950 divided by ₹10) instead of 1,00,000 units.

3. MF transactions for which stamp duty is applicable:

- Lumpsum/Upfront Purchase

- Systematic Investment Plan (SIP)

- Systematic Transfer Plan (STP)

- Switch-ins

- Dividend Reinvestment

4. MF transactions for which stamp duty is not applicable:

- Redemption

- Systematic Withdrawal Plan (SWP)

- Switch-outs

- Dividend Pay-out

5. Capital gains on stamp duty:

While computing capital gains/losses, the cost of acquisition of mutual fund units will be inclusive of the stamp duty charge.

From the earlier example, the actual cost of acquisition for calculation of capital gains will be ₹10 lakhs and not the net investment amount of ₹9,99,950.

Hence, if you sell the units for ₹9,99,980, you will incur a loss of ₹20 (₹10,00,000 – ₹9,99,980 = ₹20) and not a gain of ₹30 (₹9,99,980 – ₹9,99,950 = ₹30).

Article by

Nandini Amogh

Financial Advisor – PeakAlpha Investments